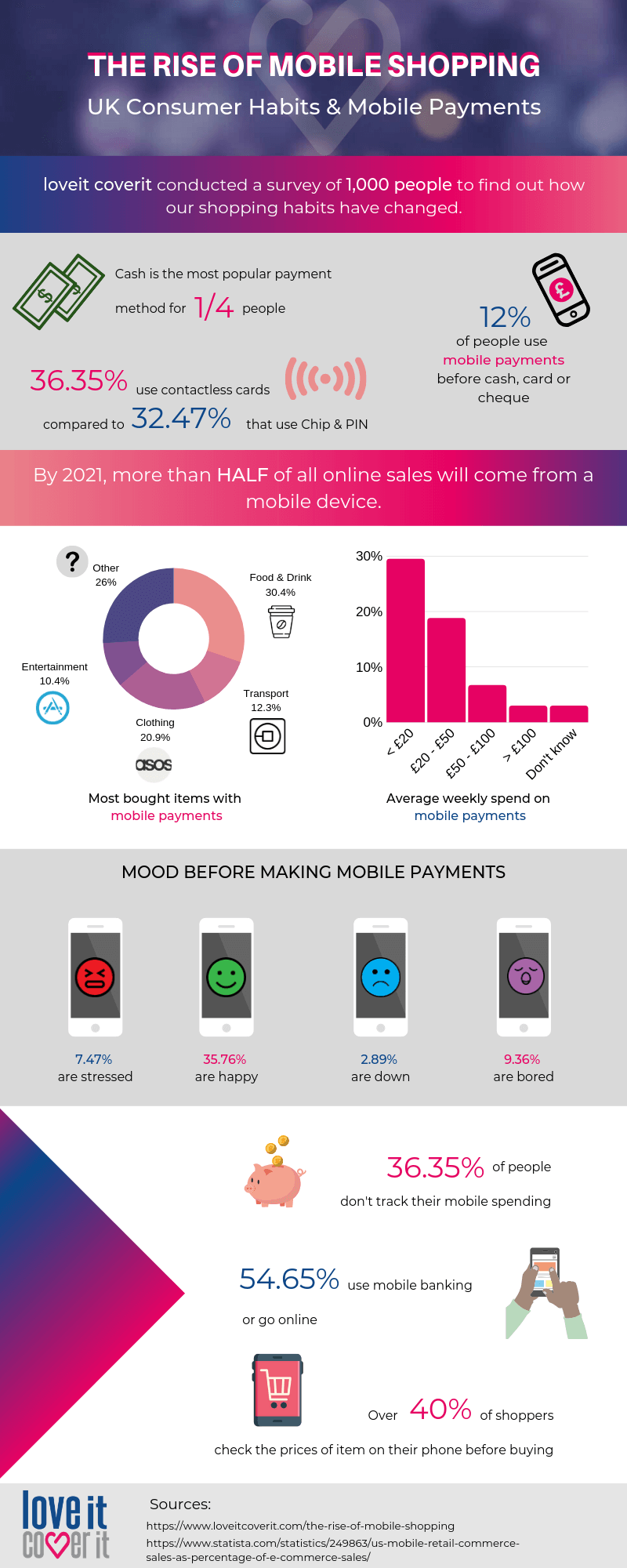

In 2018, M-commerce accounted for nearly 40% of all online shopping sales in the United States, and this is expected to grow in the next few years. Most estimates predict that by 2021, over half of all online retail will be attributed to mobile – and with the increased use of online retailers over traditional high street brands, the volume will also go up.

This demonstrates, quite clearly, how important M-commerce is to the retail landscape, and why it’s such an area of focus for existing and emerging brands. But there are myriad factors that have helped to make M-commerce into a viable option for shoppers, including the improvement in smartphone technology, the emergence of online stores such as Amazon, and the optimisation of web-shops for mobile. This, combined with customer desire for more convenient shopping options and competitive prices, has led to M-commerce becoming a dominant force in the industry.

One area in which the effect of M-commerce on retail can be truly demonstrated is with Black Friday. This annual sales event, primarily centred in America and Europe, is famous for bringing vast amounts of customers in-store, offering discounts before the Christmas rush and increasing revenue before the new year. In fact, it was estimated that 174 million shoppers in the US physically visited a store on Black Friday, in 2018.

Despite being intentionally designed to inject footfall into failing high street chains, Black Friday has also moved online, with traditional retailers having to compete with internet stores for important sales. This has, in a sense, back-fired on retailers, with many chains experiencing irregular online traffic on Black Friday which isn’t reflected in-store. For example, in 2018, Argos received half of its Black Friday orders through its website. While this is still beneficial to the retailer, it further increases the pressure on physical stores, as they struggle to generate the same sales numbers as online counterparts. Springboard, the retail data aggregator, found that footfall was down by 6% on Black Friday 2018, suggesting that it has become a more online-orientated event. This is supported by Debenhams and Superdrug, as both their websites crashed on Black Friday, with people flooding online to take advantage of deals.

While M-commerce has become a vital part of the retail sector, it has a surprisingly low approval rating. According to research done by DynamicYield, only 12% of consumers find mobile shopping convenient, which clearly shows that there is a level of dissatisfaction associated with mobile browsing. This may be due to some retailers not having the appropriate support for mobile web shopping or simply that consumers don’t trust payments through their smartphones compared to in-store shopping or using a PC. Similarly, the conversion rate of mobile shopping is far lower than any other device, with a 0.55% of searches leading to a purchase, compared to 1.54% on tablet and 2.06% on a desktop or laptop.

Apps & Mobile Reward Systems

Despite often being seen as a direct competitor to traditional retail, smartphone payments are being co-opted by some brands in order to boost audience engagement and sales. One way in which this is happening is through the use of mobile phone shopping apps, which allow customers to claim discounts, rewards, and even pay for their items.

A good example of this might be the Starbucks App, which is designed to be an all-purpose hub for customers. Not only can they see the drinks menu and get updated with special offers, it also acts as their loyalty card, allowing them to claim free drinks after they’ve spent a certain amount, and it can be used a mobile wallet that customers load money on to from their debit account. Obviously, coffee is slightly different to other products it’s much harder to just order a cup of coffee online, however, it does demonstrate how major brands are embracing smartphone technology to ensure that customers visit their stores.

To help bridge the gap between traditional retailers and M-commerce, specialist apps have been created to boost the shopping experience for customers. Yoyo partners with a variety of retailers to offer rewards and discounts, as well as informing customers when a sale is on, encouraging them to engage with their high street in new ways. It is also a mobile wallet for users, letting them load money onto the app (or link it to their Mobile Pay system), which they can then spend at partner stores. The app also acts a good market research tool for retailers, allowing them to better understand how their business is performing and letting them take steps to boost sales. In their Café Nero case study, Yoyo show that the app boosted sales and engagement with the Café Nero brand, increasing customer spend by 13% and creating 30% more unique customers.

While mobile wallets or apps may not be the answer for every failing high street, they demonstrate that by embracing M-Commerce, rather than rivalling it, brands can boost audience engagement and possibly find a new one that they couldn’t have reached before.

There is a caveat, however. That being that the sheer over-saturation of the mobile wallet market poses a threat to its effectiveness. With so many being available on the various app stores, customers are likely to become confused or frustrated as they are forced to download multiple wallets to cover all of their favourite brands. This is more likely to lead to none being used than all of them. And if every high street retailer introduced its own app, consumers would quickly become overwhelmed.

UX, Design & Optimisation

On area in which the rise of mobile shopping can really be felt is in the design and user experience of online stores. In 2018, 58% of all website visits were from a mobile device, while smartphones also made up 42% of the total time spent online. This shows a clear shift from desktop use to smartphone internet browsing – as phones become faster, more powerful, and bigger, this will only increase.

The general shift to mobile-first optimisation for websites stems from the idea of Responsive Web Design, a term coined by Ethan Marcotte in 2011. Ian Dunstan, a UX & Design expert who works on mobile web design says:

“Mobile-first started in the early 2000s as a design movement, with the focus being on designing for your smallest possible medium and scaling up to fit everything else. Since then it’s become a business movement, with retailers focussing on developing websites – specifically online stores – with mobile consumers in mind first and foremost.”

In theory, making online stores more mobile-friendly makes it easier for customers to use them without hassle, leading to a reduced bounce rate and increased sales.